The Paper Diagnostics Market is segmented by application, including infectious diseases, cancer, cardiac markers, and pregnancy. It's categorized by end-users such as clinics, hospitals, and research labs. Geographically, it covers North America, Europe & APAC: Global Size, Share, Trends, Growth and Forecast Outlook 2023-2032

Paper Diagnostics Market: Overview and Definition

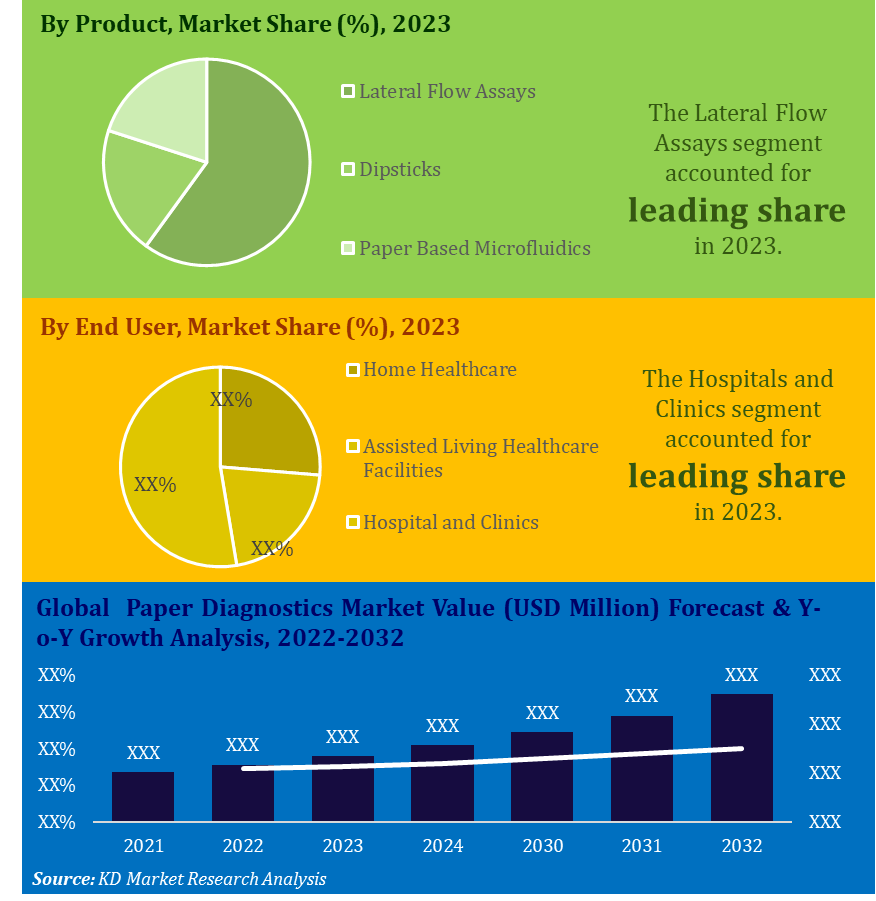

The global paper diagnostics market is projected to reach USD 7.1 billion in 2022 to USD 17.7 billion by 2032, at a CAGR of 8.5% during the forecast period 2023-2032. Due to the increased need for cost-effective healthcare in remote areas of developing countries, there is growing popularity of point-of-care diagnostic methods in these countries. Increased adoption of point-of-care diabetes test kits and pregnancy test kits is projected to favor the paper diagnostics market in developed countries.

The paper diagnostics market refers to the use of paper-based devices for medical diagnosis and monitoring of various diseases. Paper diagnostics offer advantages such as low cost, portability, ease of use, and rapid results, making them particularly useful in resource-limited settings.

The global paper diagnostics market is expected to grow significantly over the next few years due to increasing demand for affordable and accessible diagnostic tools, especially in developing countries. The market is segmented by application, product, and end user.

The application segment includes clinical diagnostics, food quality testing, and environmental monitoring. The clinical diagnostics segment is expected to dominate the market due to increasing prevalence of chronic diseases and the need for rapid and affordable point-of-care testing.

The product segment includes lateral flow assays, paper-based microfluidics, and diagnostic strips. Lateral flow assays are expected to be the largest segment due to their widespread use in a variety of diagnostic tests.

Paper Diagnostics Market: Key Drivers

The paper diagnostics market is driven by several factors, including:

Increasing prevalence of chronic diseases: The rising prevalence of chronic diseases such as diabetes, cardiovascular diseases, and cancer is driving the demand for rapid and affordable diagnostic tools. Paper diagnostics provide a low-cost, easy-to-use solution for diagnosing and monitoring these diseases, especially in resource-limited settings.

Technological advancements: Advances in technology have enabled the development of highly sensitive and specific paper-based diagnostic devices, which are capable of detecting a wide range of diseases. For instance, paper-based microfluidics technology allows for the detection of multiple disease markers simultaneously.

Growing demand for point-of-care testing: Point-of-care testing has become increasingly popular due to its ability to provide rapid and accurate results, without the need for complex laboratory infrastructure. Paper diagnostics are well-suited for point-of-care testing, as they are portable and easy to use.

Increasing demand for affordable and accessible diagnostic tools: The high cost of traditional diagnostic tools, such as PCR machines and ELISA readers, limits their use in resource-limited settings. Paper diagnostics provide an affordable and accessible alternative, making them ideal for use in low-income countries.

Rising healthcare expenditure: The global healthcare expenditure is increasing, which has led to the adoption of advanced diagnostic technologies in hospitals and clinics. Paper diagnostics offer a low-cost solution for routine diagnostic tests, allowing hospitals and clinics to allocate resources to more complex procedures.

Increasing focus on food safety and environmental monitoring: Paper-based diagnostic tools are also being used for food quality testing and environmental monitoring. The rising awareness about food safety and environmental pollution is driving the demand for rapid and affordable diagnostic tools for these applications.

Changing lifestyle habits such as smoking and unhealthy diet combined with increased incidence of obesity is anticipated to increase the prevalence of lifestyle-related disorders such as diabetes and cardiac diseases across the globe. This will lead to the development of diabetic paper diagnostic test kits in the near future, thereby driving the market. Furthermore, increased investments by the government in Research and Development related to the development of the novel in vitro diagnostics tests and devices have been thrust to the paper diagnostics market. Every year, the European Diagnostics Manufacturers Association (EDMA) invests approximately 1 billion euros in R&D of in vitro diagnostics. With the increased incidence of hospital-acquired urinary tract diseases in India and urging hospitals, doctors focus on delivering proper care and inclusion of diagnostic techniques. There is an urgent need to develop new systems and replacements, including up-grading medical infrastructure. These are also projected to influence the market positively. Moreover, there are untapped opportunities in emerging economies such as India, China, and Brazil in the field of point care diagnostics and it is also expected to boost the market.

The lateral flow assays segment accounted for more than 55% of the market's largest revenue share. The growth is due to the vast usage rate of pregnancy tests and a wide range of product-type applications. Moreover, there is a growing incidence of infectious diseases such as HIV, TB, and pneumonia, which is expected to increase the paper diagnostics market's growth. For instance, in the year 2016, there were around 2.8 million cases of TB in India. Moreover, India accounted for a quarter of the global TB cases. Also, government and healthcare organizations' efforts to create awareness about the detection and treatment of TB contribute to the growth of the paper diagnostics market. The paper-based microfluidics segment has significant growth due to the surging demand for point of care testing and Research and Development investments by life sciences and pharmaceutical organizations. For example, a self-powered, paper-based electrochemical device was developed to identify diseases such as anemia. It is a device made out of paper and helps detect biomarkers and identify diseases by performing an electrochemical analysis. The diagnostic devices market accounted the leading share of revenue in 2017. In blood separation and glucose detection, paper diagnostic devices are used. Greater flexibility and adaptability can be provided by Novel wax patterning technology, thereby increasing the diagnostics devices segment's potential.

Paper Diagnostics Market: Challenges

While the paper diagnostics market presents significant opportunities, it also faces several challenges, including:

Limited sensitivity and specificity: Paper-based diagnostic tools have limited sensitivity and specificity compared to traditional laboratory-based tests. This can result in false positives and false negatives, which can lead to misdiagnosis and inappropriate treatment.

Limited multiplexing capability: Paper-based diagnostic tools are typically limited in their ability to detect multiple disease markers simultaneously. This can be a significant limitation for complex diseases that require the detection of multiple markers.

Limited shelf life: Paper-based diagnostic tools have a limited shelf life, typically ranging from a few months to a year. This can be a significant limitation for applications that require long-term storage or use in remote locations.

Limited sample volume: Paper-based diagnostic tools typically require a small sample volume, which can limit their applicability in certain settings. For instance, some diagnostic tests require a large blood volume, which may not be possible with paper-based tools.

Quality control issues: The quality of paper-based diagnostic tools can vary significantly, which can result in inconsistent results. Quality control measures are necessary to ensure the accuracy and reliability of these tools.

Regulatory challenges: Regulatory approval can be challenging for paper-based diagnostic tools, especially in developed countries where stringent regulatory requirements are in place. This can result in delays in bringing new products to market.

Competition from established diagnostic technologies: Established diagnostic technologies, such as PCR and ELISA, have a well-established market and are widely used in clinical settings. Paper-based diagnostic tools may face significant competition from these technologies, especially in developed countries.

|

Paper Diagnostics Market : Report Scope |

|

|

Base Year Market Size |

2022 |

|

Forecast Year Market Size |

2023-2032 |

|

CAGR Value |

8.5% |

|

Segmentation |

|

|

Challenges |

|

|

Growth Drivers |

|

Paper Diagnostics Market: Segmentation

Product Outlook

- Lateral Flow Assays

- Dipsticks

- Paper Based Microfluidics

Device Type Outlook

- Diagnostic Devices

- Monitoring Devices

Application Outlook

- Clinical Diagnostics

- Cancer

- Infectious diseases

- Liver Disorders

- Other

- Food Quality Testing

- Environmental Monitoring

End-use Outlook

- Home Healthcare

- Assisted Living Healthcare Facilities

- Hospital and Clinics

Regional Outlook

- North America (The U.S. and Canada)

- Europe (U.K., Germany, France, Italy, Spain, Russia, Poland, Turkey, Switzerland, and Rest of Europe)

- Asia Pacific (Japan, China, India, Australia, South Korea, Vietnam, Philippines, Malaysia, Indonesia, Thailand, and Rest of Asia Pacific)

- Latin America (Brazil, Mexico, Columbia, Argentina, Chile, and Rest of Latin America)

- Middle East & Africa (South Africa, Saudi Arabia, UAE, Oman, Egypt, and Rest of Middle East & Africa)

Paper Diagnostics Market: Regional Synopsis

The paper diagnostics market is a global market, with significant growth potential in several regions. Here is a brief synopsis of the paper diagnostics market by region:

North America: North America is the largest market for paper diagnostics, and is expected to continue to dominate the market in the coming years. The growth of the paper diagnostics market in this region is being driven by increasing demand for point-of-care diagnostic testing, as well as advancements in paper-based diagnostic technologies.

Europe: Europe is also a significant market for paper diagnostics, and is expected to see significant growth in the coming years. The growth of the paper diagnostics market in Europe is being driven by increasing demand for affordable and accessible diagnostic tools, particularly in resource-limited settings, as well as increasing investment in research and development.

Asia-Pacific: The Asia-Pacific region is expected to see significant growth in the paper diagnostics market in the coming years. This growth is being driven by increasing demand for point-of-care diagnostic testing, particularly in developing countries, as well as advancements in paper-based diagnostic technologies.

Latin America: The Latin America paper diagnostics market is also expected to see significant growth in the coming years, driven by increasing demand for affordable and accessible diagnostic tools, particularly in resource-limited settings. However, the market is expected to face several challenges, including regulatory hurdles and limited infrastructure.

Middle East and Africa: The Middle East and Africa paper diagnostics market is also expected to see significant growth in the coming years, driven by increasing demand for point-of-care diagnostic testing, particularly in remote and underserved regions. However, the market is expected to face several challenges, including limited infrastructure and regulatory hurdles.

Paper Diagnostics Market: Key Players

- ACON Laboratories, Inc.

- Abbott

- Bio-Rad Laboratories, Inc.

- GVS S.p.A.

- Siemens Healthcare GmbH

- Diagnostics for All, Inc.

- FFEI; Navigene

- Micro Essential Laboratory Inc

- MedLife

- Kenosha Tapes

- Abcam plc

- Abingdon Health

- ACON Laboratories, Inc.

- ARKRAY, Inc.

- Other Key & Niche Players

Paper Diagnostics Market: Recent Developments

The paper diagnostics market is a rapidly growing industry, and there have been several recent developments in this space. Some of the notable developments are:

COVID-19 Pandemic: The COVID-19 pandemic has created a significant demand for rapid diagnostic tests, and paper-based diagnostic tools have emerged as a key player in this space. Several companies have developed paper-based tests for the detection of COVID-19, which are being used in both clinical and home settings.

Multiplexing Capabilities: Recent developments in paper-based microfluidics have enabled the detection of multiple analytes using a single paper-based device. This technology has significant potential for complex diagnostic applications, such as cancer diagnosis and drug discovery.

New Product Launches: Several companies have launched new paper-based diagnostic products in recent years. For example, in 2021, a company called GNA Biosolutions launched a paper-based diagnostic test for the detection of sepsis, which is a life-threatening condition.

Partnerships and Collaborations: Many companies in the paper diagnostics market are partnering with other companies and research institutions to develop new products and technologies. For example, in 2021, a company called TTP plc announced a partnership with a German research institution to develop a paper-based diagnostic tool for the detection of COVID-19.

Investment and Funding: The paper diagnostics market has attracted significant investment and funding in recent years. For example, in 2021, a company called Sensothon received funding from the European Union to develop a paper-based diagnostic tool for the detection of cancer

Need Customized Report for Your Business ?

Utilize the Power of Customized Research Aligned with Your Business Goals

Request for Customized Report- Quick Contact -

- ISO Certified Logo -

Frequently Asked Questions(FAQ)

Paper Diagnostics Market

-: Our Clients :-