Fluid Management Systems Market By Product Type (Standalone Fluid Management Systems, Integrated Fluid Management Systems, Fluid Management Disposables & Accessories); By Application (Urology and Nephrology, Laparoscopy, Gastroenterology, Gynecology / Obstetrics, Bronchoscopy, Arthroscopy, Cardiology, Neurology, Otoscopy, Dentistry, Other Applications); By End User (Hospitals, Dialysis Centers, Ambulatory Surgical Centers, Other End Users) and By Region (North America, Europe, Asia Pacific, Latin America, Middle East and Africa) - Global Market Analysis, Trends, Opportunity and Forecast, 2022-2032

Fluid Management Systems Market Size and Overview

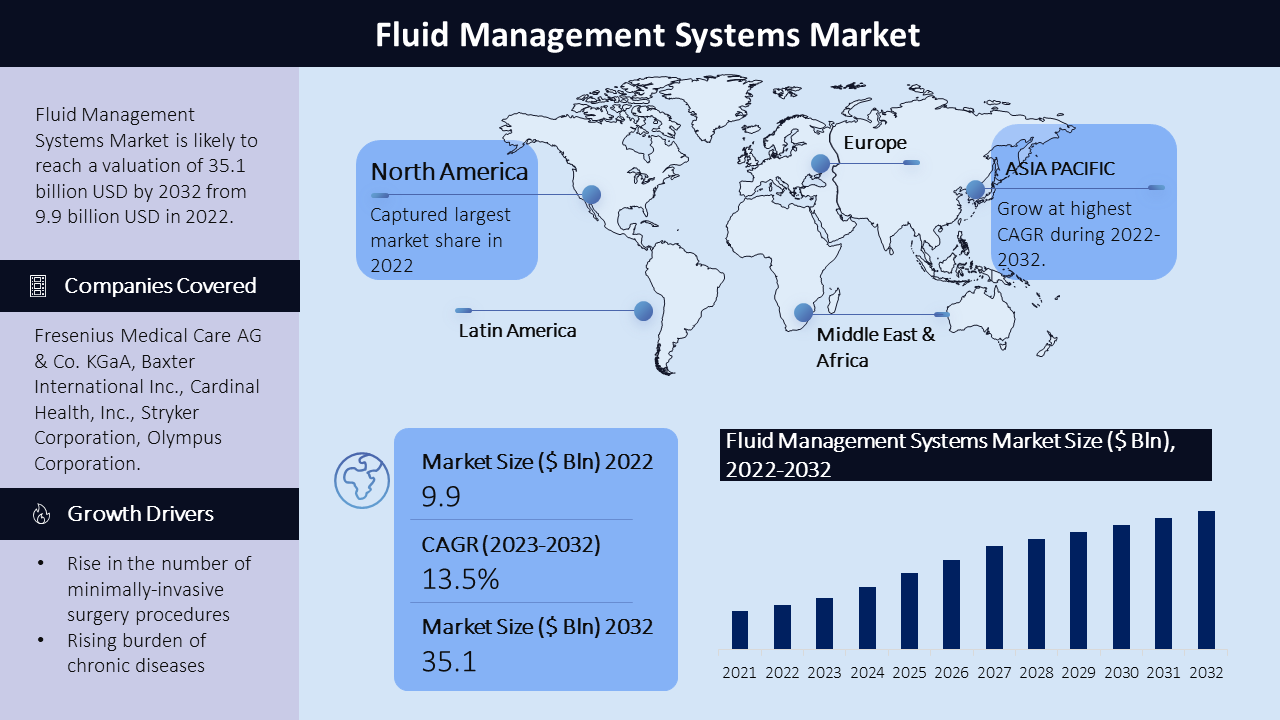

The fluid management systems market has witnessed substantial growth, achieving a significant compound annual growth rate (CAGR) of 13.5% from 2023 to 2032, with a projected revenue of USD 9.9 billion in 2022, expected to reach USD 35.1 billion by 2032. The growth of this market is driven by factors such as the increasing number of minimally invasive surgeries, advancements in fluid management systems technology, rising government funding for endosurgical procedures, and a growing number of hospitals and investments in endoscopy and laparoscopy facilities. Additionally, the rise in patients with end-stage renal disease (ESRD) and the adoption of fluid management systems for various medical procedures contribute to the market's expansion. The market encompasses a range of products, including standalone fluid management systems, integrated fluid management systems, and fluid management disposables & accessories. The market is highly competitive, with key players striving to introduce innovative solutions and capitalize on emerging opportunities in untapped markets.

|

Fluid Management Systems Market: Report Scope |

|

|

Base Year Market Size |

2022 |

|

Forecast Year Market Size |

2023-2032 |

|

CAGR Value |

13.5% |

|

Segmentation |

|

|

Challenges |

|

|

Growth Drivers |

|

Market Segmentation:

Product Type

- Standalone Fluid Management Systems

- Dialyzers

- Insufflators

- Suction/Evacuation and Irrigation Systems

- Fluid Warming Systems

- Fluid Waste Management Systems

- Others

- Integrated Fluid Management Systems

- Fluid Management Disposables & Accessories

- Catheters

- Blood Lines

- Tubing Sets

- Pressure Monitoring Lines

- Pressure Transducers

- Valves, Connectors, and Fittings

- Suction Canisters

- Cannulas

- Other Fluid Management Disposables & Accessories

Applications

- Urology and Nephrology

- Laparoscopy

- Gastroenterology

- Gynecology / Obstetrics

- Bronchoscopy

- Arthroscopy

- Cardiology

- Neurology

- Otoscopy

- Dentistry

- Other Applications

End User

- Hospitals

- Dialysis Centers

- Ambulatory Surgical Centers

- Other End Users

Geographic Regions

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Fluid Management Systems: The standalone fluid management systems segment, including dialyzers, insufflators, suction/evacuation, irrigation systems, fluid warming systems, fluid waste management systems, and others, holds a significant market share. The integrated fluid management systems and fluid management disposables & accessories also contribute to the market's growth. The laparoscopy application segment is expected to experience the highest growth during the forecast period, driven by the increasing shift towards minimally invasive procedures

Hospitals: The hospitals segment holds the largest market share in the fluid management systems market. This can be attributed to the significant number of surgical procedures performed in hospitals, driving the demand for efficient fluid management systems to ensure successful surgeries and patient outcomes.

Regional Analysis:

North America, region commands the largest share in the market, establishing itself as a lucrative and well-established market for fluid management systems. The United States plays a central role in driving the market's dominance, benefiting from technological advancements and a favorable reimbursement scenario. Moreover, the rising incidence of diseases like end-stage renal disease (ESRD) and cancer, coupled with the widespread adoption of advanced medical technologies, contributes significantly to the market's growth in North America. In Europe, countries such as Germany, France, and the United Kingdom hold substantial market shares for fluid management systems and accessories. The region's growing focus on advanced healthcare technologies and investments in medical facilities contribute to the expansion of the fluid management systems market. In the Asia Pacific region, rapid urbanization, increasing disposable incomes, and a growing appreciation for advanced healthcare facilities foster market expansion. China and India emerge as key players. The region's burgeoning middle class and demand for quality healthcare services drive the growth of fluid management systems and accessories. Latin America demonstrates steady growth, fueled by urban development, a rising middle class, and a growing demand for advanced medical treatments. Key markets in the region, such as Brazil, Mexico, and Argentina, contribute significantly to the market's upward trajectory. the Middle East and Africa exhibit a developing market with a focus on improving healthcare infrastructure and an increasing emphasis on medical treatments.

Growth Drivers:

The fluid management systems market is poised for substantial growth, driven by various factors that cater to the increasing demand for advanced medical solutions. Firstly, the rise in the number of minimally-invasive surgery procedures fuels the adoption of fluid management systems and accessories. Minimally-invasive surgeries offer numerous advantages, including fewer postoperative complications, shorter hospital stays, and reduced risks of surgical site infections. The popularity of outpatient surgeries, where patients do not require overnight hospital stays, further boosts the demand for these advanced medical technologies. Health insurance providers worldwide are increasingly covering minimally-invasive surgeries, encouraging patients and healthcare providers to opt for these procedures.

Secondly, the rising burden of chronic diseases is a significant growth driver for fluid management systems. Chronic diseases, such as end-stage renal disease (ESRD) and cancer, necessitate frequent and sophisticated medical treatments, including surgeries that require fluid management systems and accessories. The growing prevalence of chronic diseases, particularly in aging populations, propels the demand for these medical devices.

Moreover, technological advancements play a pivotal role in the market's expansion. Continuous innovations in fluid management systems have resulted in more efficient and precise medical procedures, attracting both healthcare providers and environmentally conscious consumers. These advancements also align with the increasing emphasis on sustainability and adherence to environmental regulations, driving the shift towards eco-friendly and energy-efficient equipment.

Challenges:

The lack of skilled labor poses a significant hindrance to the widespread adoption of fluid management systems and accessories. Additionally, the high cost of endosurgical procedures remains a restraint, particularly in developing countries with limited financial resources.

Key Companies:

The fluid management systems market is home to leading companies that play a crucial role in shaping the industry's landscape. Some of the prominent players in this market include Fresenius Medical Care AG & Co. KGaA, Baxter International Inc., Cardinal Health, Inc., Stryker Corporation, Olympus Corporation, B. Braun Melsungen AG, Medline Industries, Inc., KARL STORZ GmbH & Co. KG, Ecolab Inc., Smiths Medical, Zimmer Biomet Holdings Inc., Medtronic plc, FUJIFILM Holdings Corporation, CONMED Corporation, Hologic, Inc., Arthrex, Inc., Thermedx, LLC. (US), COMEG Medical Technologies, and EndoMed Systems GmbH among other players.

These companies have solidified their positions through their innovative products, extensive distribution networks, and wide-ranging product portfolios. Their competitive strategies revolve around continuous product innovation, forming strategic partnerships, engaging in mergers and acquisitions, all in pursuit of enhancing their market share and meeting the diverse needs of their customers.

In April 2022, Transit Scientific achieved a significant milestone with the FDA clearance of its XO Cross Support catheter platform for coronary use. This innovative platform is designed to guide and support the guidewire during access to the peripheral or coronary vasculature.

Similarly, in February 2022, Medtronic plc made a groundbreaking announcement about the approval of its Freezor and Freezor Xtra Cardiac Cryoablation Focal Catheters by the United States Food and Drug Administration (FDA). These catheters have become the first and only ablation catheters approved by the FDA to treat pediatric Atrioventricular Nodal Reentrant Tachycardia (AVNRT).

Need Customized Report for Your Business ?

Utilize the Power of Customized Research Aligned with Your Business Goals

Request for Customized Report- Quick Contact -

- ISO Certified Logo -

Frequently Asked Questions(FAQ)

Fluid Management Systems Market

-: Our Clients :-